DEAF Fund and Unclaimed Financial Assets in India

How Depositors, Investors, Nominees, and Legal Heirs Can Recover Forgotten Wealth

By Ashok Kakkar

In India, thousands of bank accounts, fixed deposits, insurance policies, mutual fund investments, provident fund balances, shares, and pension amounts remain unclaimed every year. Many families are unaware that money belonging to them may still be lying with banks, insurance companies, mutual funds, or government authorities.

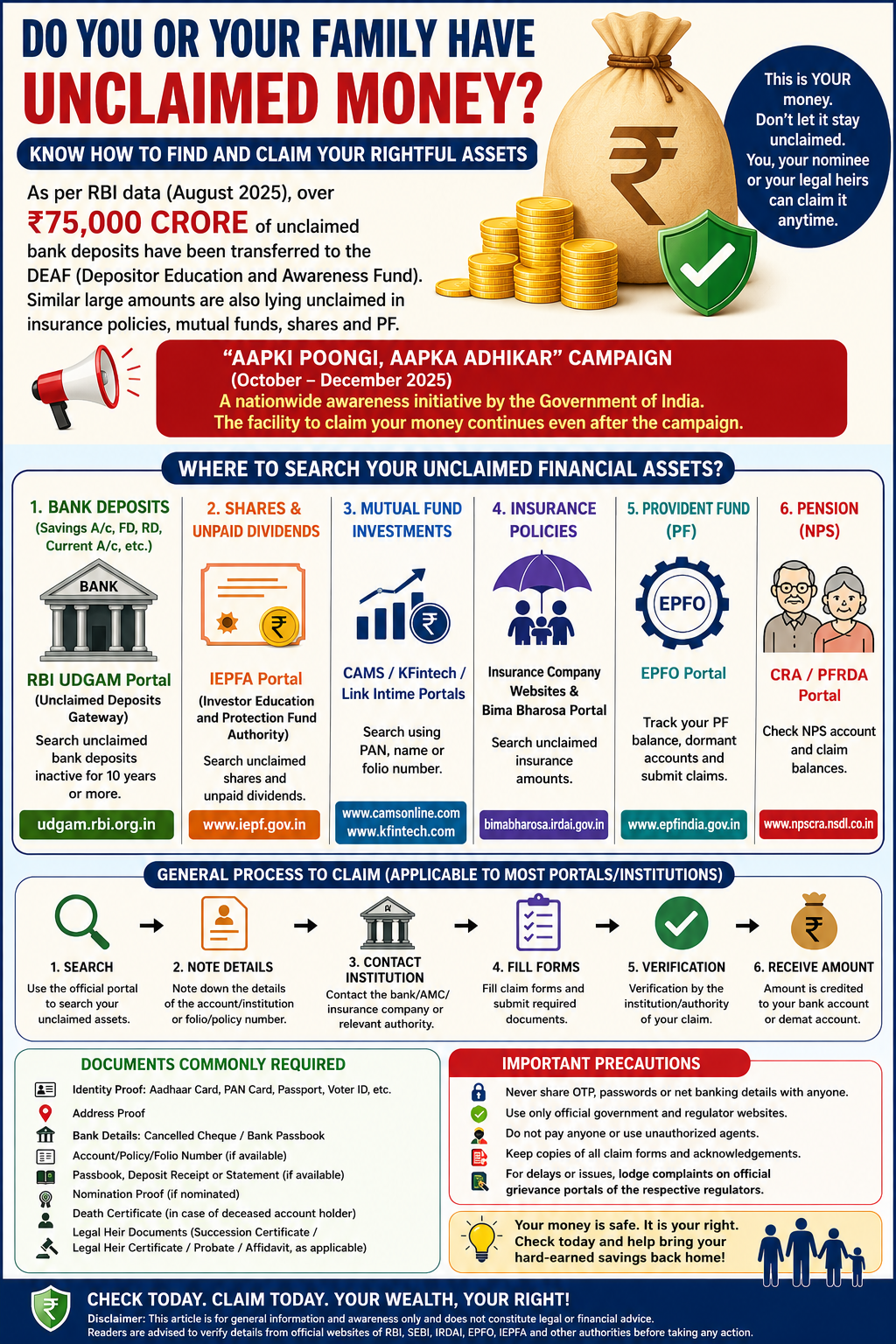

In recent years, public awareness regarding unclaimed financial assets has increased significantly. Reports indicated that more than ₹75,000 crore worth of unclaimed bank deposits had been transferred to the Depositor Education and Awareness Fund (DEAF) maintained by the Reserve Bank of India. This issue also gained public attention during the “Aapki Poongi, Aapka Adhikar” awareness campaign launched by the Ministry of Finance during 2025. Although the campaign period ended, the facility to trace and recover unclaimed financial assets continues to remain available through official platforms and regulatory systems.

This article explains the DEAF Fund, the UDGAM portal, and other important platforms through which citizens, nominees, and legal heirs can trace and recover their forgotten financial assets in India.

1. What is the DEAF Fund?

DEAF stands for Depositor Education and Awareness Fund. It was established by the Reserve Bank of India under the Banking Regulation framework for handling unclaimed bank deposits.

When bank accounts or deposits remain inoperative or unclaimed for ten years or more, banks are required to transfer such balances to the DEAF Fund maintained by RBI. These may include:

- Savings Bank Accounts

- Current Accounts

- Fixed Deposits

- Recurring Deposits

- Demand Drafts

- Other eligible unclaimed balances

However, transfer to the DEAF Fund does not mean the money is forfeited. The depositor, nominee, or legal heir continues to retain full rights over the amount.

2. Can Depositors Still Claim Money After Transfer to DEAF?

Yes. Even after transfer to the DEAF Fund:

- The original depositor can claim the amount.

- Registered nominees can submit claims.

- Legal heirs may recover the amount after completing required formalities.

The concerned bank remains responsible for verifying and settling the claim. After payment to the claimant, the bank obtains reimbursement from the DEAF Fund.

Thus, the money remains recoverable even after many years.

3. RBI UDGAM Portal for Unclaimed Bank Deposits

To simplify the process of locating dormant bank deposits, RBI introduced the UDGAM Portal.

RBI UDGAM Portal

The portal allows individuals to search unclaimed deposits across participating banks from a single platform.

Basic Process

- Register using mobile number.

- Verify OTP.

- Enter name and identification details.

- Search for unclaimed deposits.

- Identify the concerned bank.

- Contact the bank branch and submit claim documents.

The portal is especially useful for tracing old savings accounts, salary accounts, fixed deposits, or accounts belonging to deceased family members.

4. Documents Commonly Required for DEAF Claims

For Original Account Holder

- PAN Card

- Aadhaar Card

- Passbook or deposit receipt

- Bank account details

- Cancelled cheque

- Claim form

For Nominee

- Identity proof

- Nomination proof

- Death certificate of depositor

- Bank details

For Legal Heirs

- Death certificate

- Succession certificate where required

- Legal heir certificate or probate

- PAN and Aadhaar

- Affidavits or indemnity documents if prescribed by the bank

Requirements may vary depending on the bank’s internal policy and amount involved.

5. Unclaimed Insurance Policies

Many insurance claims remain unpaid because policyholders fail to update contact details or nominees are unaware of the policy.

Under regulatory guidelines, insurance companies are required to maintain searchable records of unclaimed policy amounts.

IRDAI Official Website

Bima Bharosa Portal

Most insurers also provide “Unclaimed Amount Search” facilities on their own websites.

Commonly Required Documents

- Policy number

- PAN and Aadhaar

- Identity proof

- Bank account details

- Death certificate where applicable

- Nominee proof

6. Unclaimed Shares and Dividends

Large amounts of dividends and shares remain unclaimed for years because investors forget investments or fail to update records.

Such amounts are transferred to the Investor Education and Protection Fund (IEPF).

IEPFA Portal

Basic Claim Process

- Search for unclaimed amounts.

- File Forms

- Upload required documents.

- Submit documents to the company’s Nodal Officer.

- Verification and refund process is completed.

Investors may recover both unpaid dividends and transferred shares through this mechanism.

7. Unclaimed Mutual Fund Investments

Many investors forget old mutual fund folios, dividend payouts, or redemption proceeds.

These may be traced through registrar platforms such as:

CAMS Online

KFin Technologies

Investors can generally search using:

- PAN number

- Folio number

- Name of investor

After verification, the Asset Management Company may release the unclaimed amount.

8. Provident Fund and Pension Balances

Employees frequently change jobs and may forget older PF accounts.

EPFO Portal

Using UAN credentials, members can:

- View PF balances

- Transfer old accounts

- Submit withdrawal claims

- Trace dormant balances

Similarly, pension-related claims may be processed through relevant pension authorities or NPS service providers.

9. Important Precautions While Claiming Unclaimed Assets

While tracing financial assets, individuals should remain cautious.

Important Safety Measures

- Use only official portals and websites.

- Never share OTPs or banking passwords.

- Avoid unauthorized agents demanding advance fees.

- Maintain copies of claim forms and acknowledgements.

- Verify claim procedures directly from official authorities.

If a bank or institution delays processing, grievance mechanisms of RBI, IRDAI, SEBI, EPFO, or IEPFA may be used.

10. Importance for Legal Heirs and Families

In many cases, legal heirs are unaware of financial assets left behind by deceased family members. Lack of nominations, missing records, or outdated addresses often create difficulties.

Families should therefore:

- Maintain proper financial records.

- Register nominees in all accounts and investments.

- Periodically review dormant investments.

- Inform family members about major financial assets.

A simple review of old documents, emails, passbooks, insurance papers, or tax records may help identify forgotten wealth.

Conclusion

Unclaimed financial assets are not merely inactive numbers in institutional records; they represent the hard-earned savings of ordinary citizens and families. Whether the amount relates to a dormant bank account, forgotten fixed deposit, unpaid insurance claim, mutual fund investment, provident fund, or old shareholding, rightful owners continue to retain legal rights over such assets.

The DEAF Fund, RBI UDGAM Portal, IEPFA mechanism, insurance search facilities, mutual fund registrars, and EPFO systems have significantly simplified the process of tracing and recovering unclaimed money.

A few minutes spent checking these official portals today may help recover valuable financial assets tomorrow.

Disclaimer

This article is intended solely for educational and public awareness purposes. Rules, procedures, claim requirements, and regulatory guidelines may change from time to time. Readers are advised to verify the latest information directly from RBI, IRDAI, SEBI, IEPFA, EPFO, banks, insurers, mutual fund registrars, and other competent authorities before taking any action. Professional legal or financial advice should be obtained wherever necessary.

Ashok Kakkar

#DEAFFund #UnclaimedDeposits #RBIUDGAM # FinancialAwareness #BankDeposits #IEPFA#EPFO #InsuranceClaims #MutualFunds #LegalHeirs