A Practical Guide for Borrowers, Bankers, Chartered Accountants, and Property Advisors

Introduction

For most individuals, repaying a home loan is a major financial milestone. After years of regular EMI payments, receiving the final loan closure confirmation often brings a sense of relief and achievement. However, many borrowers assume that once the loan account is closed, all obligations related to the property automatically come to an end.

In reality, loan repayment is only the financial closure of the transaction. Several legal, documentation, and compliance-related formalities still need attention. If these post-closure steps are ignored, borrowers may face difficulties during property sale, refinancing, title verification, inheritance planning, or future legal scrutiny.

Many property disputes and transaction delays arise not because the loan remains unpaid, but because the records relating to the mortgage or charge over the property were never properly updated after repayment.

This article explains the important post-home-loan closure steps that every borrower and advisor should consider to ensure complete and hassle-free closure of the loan transaction.

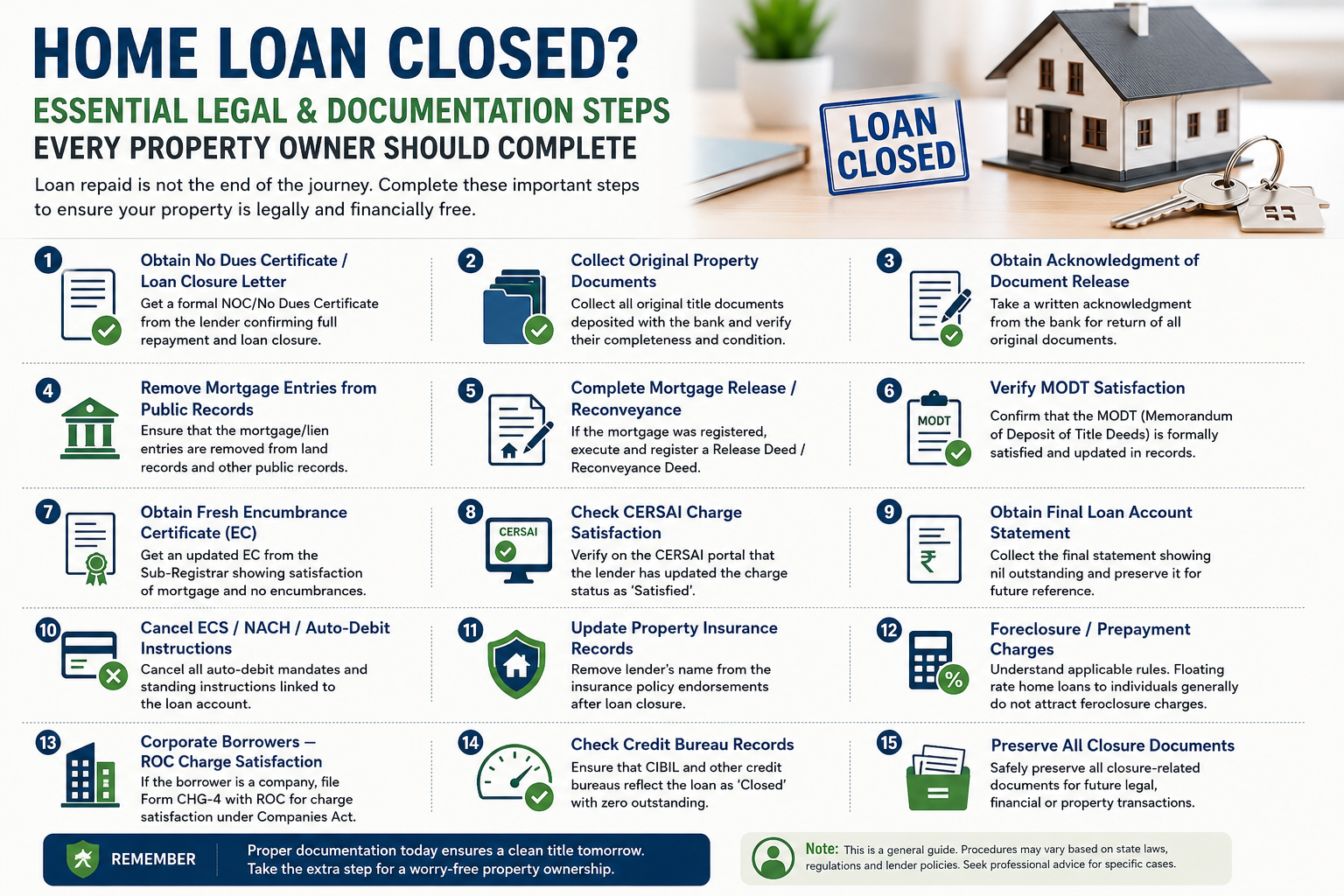

1. Obtain a No Dues Certificate or Loan Closure Letter

The first and most important document to obtain after loan repayment is the No Dues Certificate (NDC), No Objection Certificate (NOC), or Loan Closure Letter issued by the bank or housing finance company.

This document confirms that:

- The entire loan has been repaid.

- No amount remains outstanding.

- The lender has no further financial claim on the property.

- The loan account stands closed.

Borrowers should verify that the certificate contains correct details of the borrower, loan account number, property particulars, and closure date.

Both physical and digital copies should be preserved carefully for future reference.

2. Collect All Original Property Documents

When a home loan is sanctioned, banks usually retain original title documents as security.

After closure of the loan:

- Collect all original documents deposited with the lender.

- Verify that every document has been returned.

- Check the condition and completeness of each document.

- Compare the documents with the original submission list.

Missing title documents can create significant problems during future sale or transfer of the property. Therefore, document verification should be done immediately at the time of collection.

3. Obtain Written Acknowledgment of Document Release

While collecting the original documents, borrowers should also obtain a formal acknowledgment or release letter from the lender.

The document should mention:

- Details of documents returned.

- Date of release.

- Name and designation of authorized bank official.

- Borrower’s acknowledgment of receipt.

This serves as evidence in case any dispute arises regarding missing documents in the future.

4. Ensure Removal of Mortgage Entries from Public Records

In several states, details of mortgages or liens are reflected in land records, revenue records, or other government databases.

After loan closure, borrowers should ensure that:

- The lender has issued the necessary release confirmation.

- Relevant authorities have updated their records.

- Mortgage-related entries no longer appear as active encumbrances.

Failure to update these records may create confusion regarding ownership rights and property valuation.

5. Complete Mortgage Release or Reconveyance Formalities

Where the mortgage was created through a registered instrument, repayment alone may not automatically remove the lender’s charge.

In such cases, a Release Deed, Reconveyance Deed, or similar document may need to be executed and registered before the Sub-Registrar.

This legal step formally records that the lender’s interest in the property has been extinguished.

Borrowers should seek professional advice whenever registered mortgages are involved.

6. Verify Closure of MODT Registration

In many states, housing loans are secured through a Memorandum of Deposit of Title Deeds (MODT), which may be registered with the Sub-Registrar.

After repayment, borrowers should verify that:

- The MODT has been appropriately satisfied.

- Necessary filings have been completed.

- Search reports do not reflect any continuing encumbrance.

This step is often overlooked but becomes extremely important during future title verification exercises.

7. Obtain a Fresh Encumbrance Certificate

An Encumbrance Certificate (EC) provides evidence regarding registered transactions affecting a property.

Once the loan is repaid and mortgage satisfaction formalities are completed, obtaining a fresh EC is advisable.

The updated EC should ideally show:

- Satisfaction of the mortgage.

- Absence of active encumbrances relating to the loan.

- Clean title position.

Prospective buyers, banks, and legal advisors frequently rely on ECs during due diligence.

8. Verify CERSAI Charge Satisfaction

Most secured loans today are registered with the Central Registry of Securitisation Asset Reconstruction and Security Interest (CERSAI).

After repayment:

- The lender should update the CERSAI records.

- The charge should reflect as satisfied or closed.

- Borrowers should independently verify the status.

An active charge appearing in CERSAI records despite loan closure may create unnecessary hurdles during future borrowing or property transactions.

9. Obtain the Final Loan Account Statement

A complete loan statement should be obtained and preserved after closure.

The statement helps in:

- Verifying repayment history.

- Confirming nil outstanding balance.

- Resolving future accounting issues.

- Supporting audit and tax records where required.

Professionals advising clients should ensure that no residual charges or pending entries remain in the account.

10. Cancel ECS, NACH, and Auto-Debit Instructions

Most home loans operate through automated payment mechanisms such as:

- ECS mandates

- NACH instructions

- Standing instructions

- Auto-debit arrangements

After closure of the loan, these mandates should be formally cancelled.

Ignoring this step could result in accidental debits or reconciliation disputes at a later stage.

11. Update Property Insurance Records

Many housing loans require property insurance, and the lender’s interest is often noted in the insurance policy.

After loan closure:

- Request modification of policy endorsements.

- Remove the lender’s name where appropriate.

- Ensure future claims are processed directly in favour of the property owner.

Proper updating of insurance records helps avoid procedural complications during claim settlement.

12. Understand Foreclosure and Prepayment Issues

Borrowers who repay their loans before the scheduled tenure should verify whether any foreclosure or prepayment charges apply.

Regulatory guidelines generally provide protection to individual borrowers in floating-rate housing loans. However, treatment may vary depending on:

- Loan type.

- Interest rate structure.

- Borrower category.

- Terms of sanction.

Reviewing the sanction letter and applicable regulatory provisions remains important.

13. Corporate Borrowers Must Ensure Charge Satisfaction with ROC

Where a company has borrowed against property and registered a charge with the Registrar of Companies (ROC), additional compliance is necessary.

The charge satisfaction process must be completed through the prescribed filings under the Companies Act.

Failure to update ROC records may continue to show an active charge, affecting:

- Future borrowing arrangements.

- Investor due diligence.

- Mergers and acquisitions.

- Corporate restructuring exercises.

Chartered Accountants and company advisors should pay particular attention to this requirement.

14. Check Credit Bureau Records

After closure of the home loan, borrowers should review their credit reports from major credit information companies.

The report should correctly show:

- Loan status as closed.

- Zero outstanding balance.

- No overdue amount.

Incorrect reporting may negatively affect future credit eligibility and credit scores.

A review within a few months of closure is generally advisable.

15. Preserve All Closure Documents Safely

Property transactions often come under scrutiny many years after loan closure.

Therefore, borrowers should permanently preserve:

- No Dues Certificate

- Loan Closure Letter

- Original title documents

- Release or Reconveyance Deed

- Updated Encumbrance Certificate

- CERSAI satisfaction confirmation

- Final loan account statement

- Insurance endorsement records

Maintaining an organized record file can prevent future legal and procedural difficulties.

Conclusion

Repayment of a home loan marks the end of a financial liability, but it should not be treated as the end of the overall process. True closure occurs only when all legal, documentary, regulatory, and registry-related formalities have been completed.

A property free from financial encumbrances and supported by proper documentation provides greater security, smoother future transactions, and stronger legal protection.

Borrowers, Chartered Accountants, advocates, bankers, and property advisors should therefore view home loan closure as a structured process involving both repayment and documentation compliance. Taking a little extra care at this stage can save considerable time, cost, and inconvenience in the future.

Disclaimer

This article is intended solely for educational and informational purposes. Procedures relating to mortgage release, registration requirements, CERSAI updates, and other compliance matters may vary depending upon applicable laws, state regulations, lender policies, and subsequent regulatory amendments. Readers should seek professional legal, financial, or tax advice before acting upon any specific matter.