From Debt Recovery to Business Resolution: Understanding the Impact of IBC on India’s Recovery Framework

Introduction

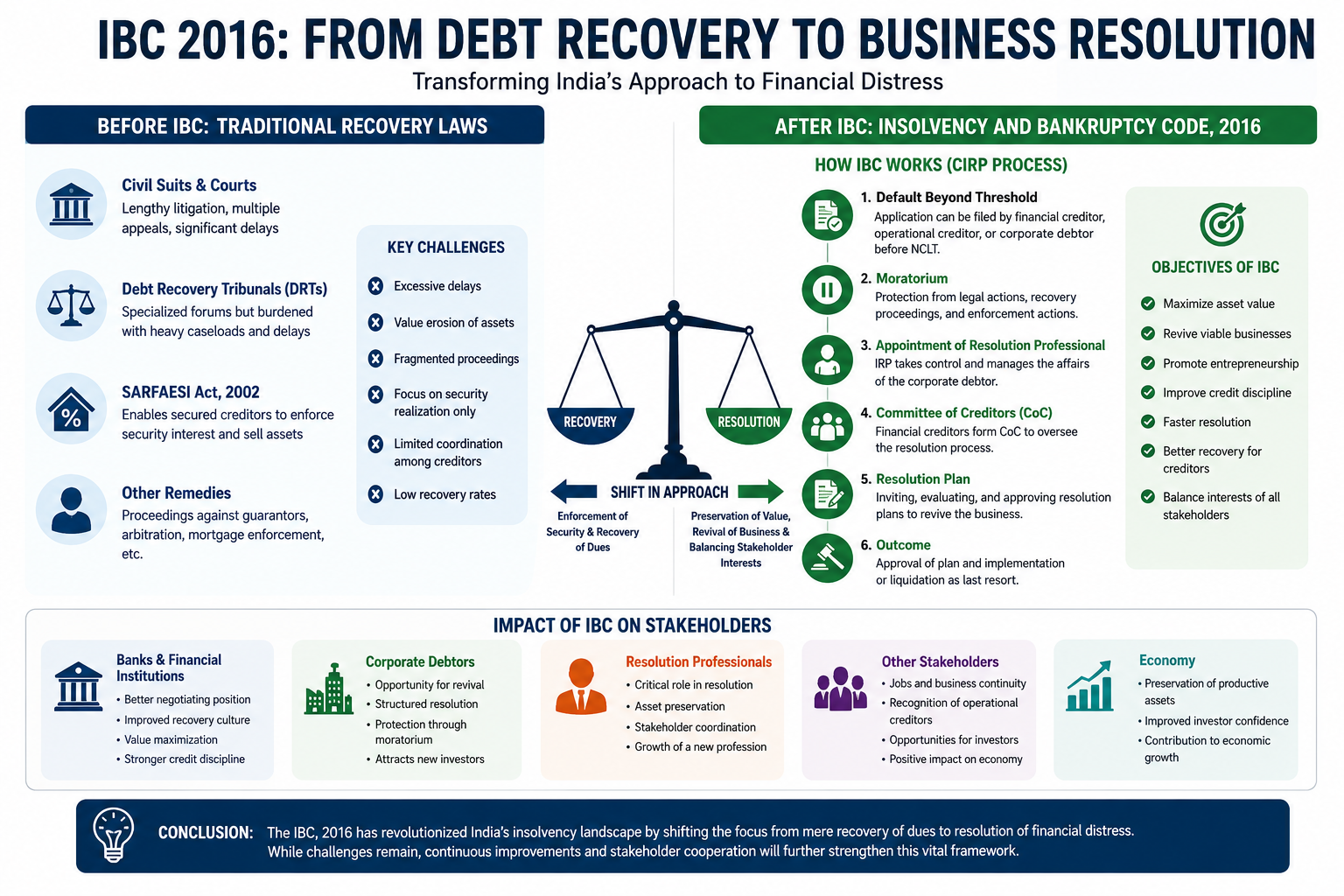

The banking system plays a vital role in the growth of any economy by providing financial support to businesses and individuals. However, not all loans are repaid on time. When borrowers fail to service their debts and loan accounts become Non-Performing Assets (NPAs), banks and financial institutions must take steps to recover their dues.

Before the enactment of the Insolvency and Bankruptcy Code (IBC), 2016, banks largely depended upon traditional recovery laws such as civil suits, Debt Recovery Tribunals (DRTs), SARFAESI proceedings, and other legal remedies. While these mechanisms provided avenues for recovery, they often faced practical challenges such as delays, fragmented proceedings, multiple litigations, and erosion of asset value.

The introduction of the Insolvency and Bankruptcy Code, 2016 marked a significant shift in India’s recovery and insolvency landscape. It moved the focus from mere recovery of debt to resolution of financial distress and preservation of business value.

This article provides a simple overview of the traditional recovery framework, the reasons behind the introduction of IBC, its objectives, performance, and its impact on banks, financial institutions, resolution professionals, stakeholders, and corporate debtors.

1. Recovery Framework Before IBC

Prior to 2016, lenders had several legal remedies available for recovering their dues.

(A) Civil Recovery Suits

Banks could file civil suits before courts for recovery of outstanding amounts. However, civil litigation often involved lengthy procedures and substantial delays.

(B) Debt Recovery Tribunals (DRTs)

The Recovery of Debts and Bankruptcy Act established DRTs for faster adjudication of claims by banks and financial institutions.

The objective was to provide a specialized forum for recovery matters. Although DRTs improved the process to some extent, increasing caseloads and procedural challenges often resulted in delays.

(C) SARFAESI Act, 2002

The SARFAESI Act empowered secured creditors to enforce security interests without requiring court intervention at the initial stage.

Under this Act, banks could:

- Take possession of secured assets.

- Manage secured assets.

- Sell secured assets.

- Recover dues from collateral security.

The SARFAESI Act became one of the most effective recovery tools available to secured lenders.

(D) Other Legal Remedies

Banks also relied upon:

- Arbitration proceedings.

- Proceedings under guarantee agreements.

- Recovery actions against guarantors.

- Enforcement of mortgages and pledged assets.

2. Challenges in the Traditional Recovery System

Although several recovery mechanisms existed, they suffered from various practical limitations.

(A) Excessive Delays

Recovery proceedings often continued for years due to litigation, appeals, and procedural requirements.

(B) Asset Value Erosion

By the time recovery proceedings concluded, the value of assets frequently deteriorated significantly.

(C) Fragmented Proceedings

Different creditors often initiated separate actions before different forums, resulting in duplication and inefficiency.

(D) Focus on Security Rather Than Business

Traditional laws primarily focused on realization of security rather than revival of the business.

(E) Limited Coordination Among Creditors

Multiple lenders often pursued independent recovery actions, reducing the possibility of achieving an optimal outcome.

(F) Low Recovery Rates

In many cases, banks recovered only a fraction of the outstanding dues after prolonged litigation.

These challenges highlighted the need for a comprehensive insolvency framework capable of addressing financial distress in a more structured manner.

3. Why Was the IBC Introduced?

The Insolvency and Bankruptcy Code, 2016 was introduced to create a unified and time-bound framework for insolvency resolution.

The primary objectives included:

- Maximization of asset value.

- Revival of viable businesses.

- Promotion of entrepreneurship.

- Improvement of credit discipline.

- Faster resolution of stressed assets.

- Better recovery for creditors.

- Balancing interests of all stakeholders.

The Code represented a major reform in India’s financial and legal ecosystem.

4. The Fundamental Shift: Recovery vs Resolution

One of the most important contributions of IBC is the change in approach from “Recovery” to “Resolution.”

Traditional Recovery Approach

The focus was largely on:

- Selling collateral.

- Enforcing securities.

- Recovering dues from borrowers and guarantors.

Resolution Approach under IBC

The focus shifted towards:

- Preserving enterprise value.

- Keeping viable businesses operational.

- Finding new investors.

- Restructuring debt.

- Protecting employment.

- Maximizing value for stakeholders.

This change in philosophy transformed the manner in which financial distress is addressed in India.

5. How the IBC Process Works

When a corporate debtor commits a default beyond the prescribed threshold under the Insolvency and Bankruptcy Code (IBC), insolvency proceedings may be initiated before the National Company Law Tribunal (NCLT). Such proceedings can be filed not only by eligible financial creditors and operational creditors but also voluntarily by the corporate debtor itself when it is unable to meet its financial obligations. Upon admission of the application, the Corporate Insolvency Resolution Process (CIRP) commences with the objective of exploring the possibility of resolving financial distress and preserving the corporate debtor as a going concern.

After admission:

Step 1: Moratorium

A moratorium is imposed, preventing recovery actions, litigation, and enforcement proceedings.

Step 2: Appointment of Resolution Professional

An Insolvency Professional takes charge as Interim Resolution Professional and later as Resolution Professional.

Step 3: Committee of Creditors (CoC)

Financial creditors form the Committee of Creditors which supervises the resolution process.

Step 4: Invitation of Resolution Plans

Potential investors and applicants submit resolution plans for revival of the company.

Step 5: Approval of Plan

If approved by the CoC and NCLT, the resolution plan is implemented.

Step 6: Liquidation

If resolution is not possible, the company may proceed to liquidation.

6. Impact of IBC on Banks and Financial Institutions

The introduction of IBC has significantly influenced lending and recovery practices.

Positive Outcomes

(A) Improved Recovery Culture

Borrowers became more conscious of repayment obligations due to the consequences of insolvency proceedings.

(B) Better Negotiating Position

The possibility of losing management control often encourages settlement discussions.

(C) Value Maximization

In many cases, businesses are sold as going concerns, generating better value than piecemeal asset sales.

(D) Enhanced Credit Discipline

IBC has strengthened overall credit behaviour in the financial system.

Challenges

- Delays in some large cases.

- Significant haircuts in certain resolutions.

- Capacity constraints before adjudicating authorities.

7. Impact on Corporate Debtors

IBC has changed the position of corporate borrowers considerably.

Benefits

- Opportunity for business revival.

- Structured debt resolution.

- Protection through moratorium.

- Possibility of attracting new investors.

Concerns

- Loss of management control.

- Increased scrutiny of transactions.

- Risk of liquidation if resolution fails.

Nevertheless, the Code offers a better chance of business survival compared to immediate asset liquidation.

8. Impact on Resolution Professionals

The IBC created a completely new professional ecosystem.

Resolution Professionals now play a critical role in:

- Managing distressed companies.

- Preserving assets.

- Conducting CIRP processes.

- Coordinating with creditors.

- Evaluating claims.

- Supporting implementation of resolution plans.

The profession has emerged as a specialized field requiring legal, financial, accounting, and management expertise.

9. Impact on Other Stakeholders

Employees

Successful resolution helps preserve jobs and business continuity.

Operational Creditors

Operational creditors receive recognition within the insolvency process and participate through statutory mechanisms.

Investors

The framework provides opportunities to acquire stressed businesses and revive them.

Economy

Successful resolutions preserve productive assets and contribute to economic growth.

10. Has the IBC Achieved Its Objectives?

After nearly a decade of implementation, the IBC has undoubtedly transformed India’s insolvency ecosystem.

Some notable achievements include:

- Establishment of a unified insolvency framework.

- Improved credit discipline.

- Greater transparency in recovery processes.

- Increased focus on business revival.

- Enhanced stakeholder participation.

- Development of a professional insolvency ecosystem.

However, certain challenges remain:

- Delays in some cases.

- Litigation at various stages.

- Capacity constraints in adjudicating authorities.

- Need for continuous reforms and procedural improvements.

Despite these challenges, the IBC is widely regarded as one of India’s most significant economic and legal reforms.

Conclusion

The journey from traditional debt recovery laws to the Insolvency and Bankruptcy Code represents a fundamental transformation in India’s approach to financial distress. Earlier recovery mechanisms primarily focused on enforcement of security and recovery of dues, whereas the IBC seeks to preserve enterprise value, revive viable businesses, and maximize returns for stakeholders through a structured and collective process.

While traditional laws such as DRT and SARFAESI continue to play an important role in the recovery framework, the IBC has introduced a broader objective of business resolution and economic value preservation. Together, these mechanisms form an integrated recovery ecosystem that supports both creditor rights and business continuity.

As India’s banking and financial sector continues to evolve, the success of the insolvency framework will depend upon timely resolution, stakeholder cooperation, professional expertise, and continuous regulatory improvements.

Disclaimer

This article is intended solely for educational and general awareness purposes. The Insolvency and Bankruptcy Code, 2016, SARFAESI Act, DRT framework, and related laws contain detailed provisions, rules, regulations, judicial interpretations, and amendments that may change from time to time. Readers should refer to the latest statutory provisions, regulatory guidelines, and professional advice before taking any decision. The article provides only a broad introductory overview and should not be construed as legal, financial, or professional advice.

Ashok Kakkar

#Banking and Finance #NPA Recovery #SARFAESI Act #Debt Recovery Tribunal (DRT) #Resolution Professional #Corporate Debt Resolution #IBC 2016 #Insolvency Law #Financial Creditors # Corporate Debtor #NCLT